Evaluating a Stable Value Fund

Stable value funds have played a key role in defined contribution plans for nearly a half century, and plan sponsors now have more options than ever. With more than 50 solutions to choose from across a range of providers and product types, how do you identify the best stable value option for your plan?1

Below we cover the things you should know, and address some of the most commonly asked questions around evaluating and selecting a stable value fund.

Why do plan sponsors offer stable value funds?

Plan sponsors are required to offer a principal preservation or safe investment option to meet the requirements of 404(c). Stable value has long been the most widely used principal preservation option within defined contribution retirement plans.

Stable value offers protection from market volatility while providing principal protection and a guaranteed interest rate. Liquidity for participant-initiated activity is available on a daily basis at book value. These funds package a portfolio of high-quality, short- to intermediate-duration bonds with an insurance “wrapper.” This wrap, provided by an insurance company or a bank, guarantees principal and accumulated interest regardless of what happens in the market.

Also, plan advisors overwhelmingly recommend stable value. Our latest study found that 82% of plan sponsors said their advisor recommended stable value — and 90% of those plan advisors said outperformance compared to money market funds was a key reason.2

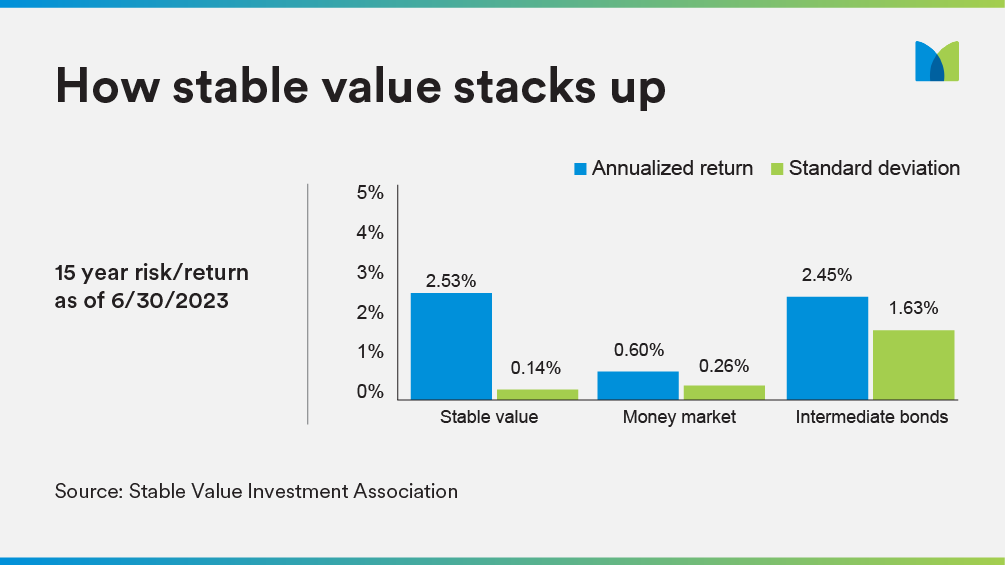

How does stable value’s historical performance compare to other principal preservation options?

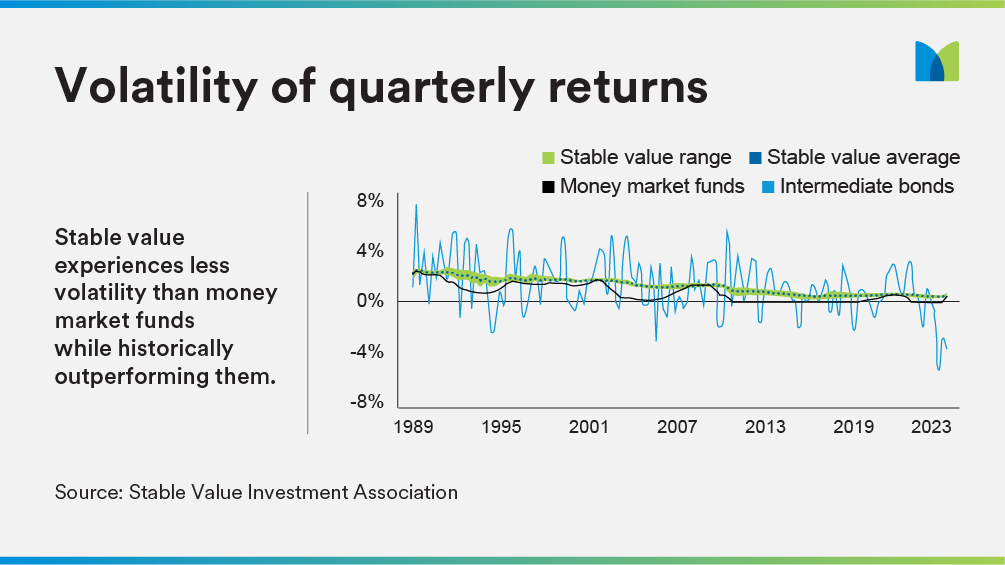

The best way to think about stable value returns is to compare them to those of other capital preservation options, such as money market funds. Over the past 15 years, stable value funds have had significantly higher annualized returns compared to money market funds. Stable value has a return profile comparable to intermediate bonds but with a standard deviation lower than money market funds.

What are 5 key criteria for evaluating stable value funds?

Plan sponsors should evaluate a number of factors when choosing a stable value fund, including underlying performance, historical net crediting rates, historical market-to-book ratios, expenses, and exit provisions.

Performance

The more consistent the performance of a stable value fund, the better. When comparing returns, make sure to look at multiple time periods, including one-, three-, five- and 10-year returns. You will want to see:

- Consistent performance with a demonstrated track-record

- Funds that consistently outperform their peers

- Funds offered by companies with a core competency in stable value , such as MetLife.

Historical net crediting rates

When evaluating net crediting rates, there are a number of factors to consider. While a higher crediting rate might sound more attractive, it should be considered against all other factors. Consider the underlying investment portfolio that supports the crediting rate, including the benchmark and duration of the portfolio, as well as the credit quality of the securities. The higher rate may be attributed to a portfolio with a higher risk profile. Funds from reliable providers may include a lower net crediting rate — but that lower rate may come with decreased return volatility.

Historical market-to-book ratios

Stable value funds are typically comprised of a portfolio of bonds. The market value of the fund’s holdings fluctuates as interest rates rise and fall. Bonds have an inverse relationship with interest rates. When rates go down, the market value of those securities goes up. And the opposite is true: When rates go up, the value of the securities goes down. Stable value funds smooth market volatility and are designed to have market value ratios that are at times below 100% and at times above 100%.

In general, a fund’s market-to-book ratio should be evaluated relative to the prevailing market environment and other stable value funds, rather than as a stand-alone measure.

Expenses

There can be a range of fees associated with different stable value solutions. It is important to understand a fund’s expense ratio and the benefits derived for the fees paid. For example, some solutions are invested in an insurer’s general account and may not provide the same level of transparency as other solutions such as collective investment trusts (CIT) or separate accounts. A lower fee does not necessarily mean a better outcome for participants. Therefore, an analysis should consider expenses in the context of the net return to participants.

Exit Provisions

It is also important to understand a fund’s exit or termination provision and the impact that has on the structure of the fund. Stable value funds can have a variety of exit provisions including a 12-month put at book value, the lower of market or book value, or installments over a period of time. The most common exit provision is the 12 -month put at book value.

This enables a plan to exit the fund at full book value upon 12 months’ advance notice. The lesser of book or market value allows a plan to exit the fund at any time. The value the plan would receive upon exit is the lower of the book or market value. If market value is below book value, a plan can wait until market equals book and exit immediately at that time if they so choose.

Other solutions, such as insurance company evergreen general account funds, provide for a series of installment payouts at book value. A typical example would be five annual installments to complete the termination process. Because 12-month put funds require a full book value payment in only 12 months, they tend to have a shorter investment duration, typically two to three and a half years.

The lesser of market or book value funds tend to have a longer investment duration, since plans cannot receive a book value payment unless the market value of the assets is at or above the book value. Likewise, insurance company general account funds tend to have a longer investment duration, since any exit from the fund would be paid out over a series of installments, often extending out five years.

Many stable value funds have a “portability” feature which allows the plan to stay invested in the fund when moving to a new recordkeeper, rather than having to exit and reinvest the assets in a new fund. The biggest benefit of this feature is the plan sponsors’ flexibility in selecting a new record keeper.

How do stable value funds respond to changes in interest rates?

The price of bonds, the core stable value investment, moves in the opposite direction as changes in interest rates. As interest rates rise, the market value of existing bonds goes down. As interest rates fall, the market value of existing bonds goes up. Since stable value amortizes the market value gains and losses through the crediting rate reset formula, stable value rates tend to lag the movement of market rates both up and down.

Why is a stable value provider's track record important?

A stable value fund’s track record is an indicator of its ability to perform in various market conditions. It’s important to look at various intervals of that record — such as one, three, five and 10 years — for a more complete picture. It’s also important to look at the track record and experience of the entities that comprise the fund, such as the fund sponsor, asset managers and wrap providers.

How do you evaluate a stable value fund that’s new to the market?

New funds may have little-to-no track record. A proxy for a new fund’s track record is the experience and historical performance of the investment manager in the investment mandate they are managing in the fund. The experience, size and demonstrated track record of the wrap provider(s) is also important.

When considering a new stable value fund, look at who is sponsoring the fund, who is managing the underlying assets and who is providing the insurance wrap. If each of these parties have track records of consistent performance and reliability, that’s a strong signal that the new fund may perform well.

How do you evaluate the underlying investments in a stable value fund?

Plan sponsors may not need intricate knowledge of a fund’s underlying bond portfolio but should have an overall understanding of the investment philosophy, duration, permissible holdings, and overall credit quality. If you have evaluated the fund’s performance relative to other stable value funds, historical net crediting rates , market-to-book ratios, expenses, and exit provisions, you have everything you need to make an informed choice. The same holds true for new funds; while they may not have historical data points available for market-to-book and net crediting rates, evaluating the fund sponsor, asset manager, wrap provider, expenses and exit provision will aid your evaluation process.

MetLife’s stable value solutions

Stable value is a core competency of MetLife, our financial strength ratings are among the highest in the industry.3 Our extensive expertise managing both assets and liabilities, and our 150-year heritage of financial stability and strength, make us the preferred provider for many stable value managers and retirement plan sponsors. To learn more about our stable value solutions please contact our stable value team at (833) 948-2275.

1 https://www.fi360.com/what-we-do/software-technology/fi360-stable-value-vision

3 For current ratings information, visit www.metlife.com and click on “About Us” and then “Company Ratings.”

All guarantees are subject to the financial strength and claims-paying ability of the issuing MetLife company.

Group annuity contracts are issued by one of the following MetLife, Inc. companies: Metropolitan Life Insurance Company, New York NY; and Metropolitan Tower Life Insurance Company, Lincoln, NE; and are distributed by MetLife Investors Distribution Company (“MLIDC”) (member FINRA). All are MetLife companies. Like most group annuity contracts, MetLife group annuities contain certain limitations, exclusions and terms for keeping them in force. Ask a MetLife representative for costs and complete details.