You’ve heard it here before, but it bears repeating: Over time, stable value consistently outperforms every other type of defined contribution (DC) capital preservation product, including money market funds and bank demand deposit accounts. Increasingly, plan sponsors and consultants have realized that stable value can add participant value not only in a capital preservation option, but in balanced and target date funds as well. In this article, we are going “under the hood” to show how the stable value “engine” achieves such remarkable results.

What is the stable value engine?

What we call the stable value “engine” are contracts with provisions that allow plans to hold the assets supporting the contract at “book value.” Accounting rules allow book value accounting only for contracts with the required provisions issued to participant-directed DC plans. “Book value” allows securities to be held at the price paid for them plus interest at a rate determined by contract rules regardless of the market value of the securities. As a result, participant transactions (withdrawals, transfers, loans, etc.) occur at book value and, because a stable value crediting rate cannot be negative, book values cannot decline. That means that the value that participants see on their statements can only decline because of withdrawals.

Participant values do not change because of day-to-day changes in the securities’ markets. Stable value smooths out the underlying market volatility by resetting the crediting rate periodically, typically quarterly. The crediting rate amortize market value gains and losses over time.

How it works

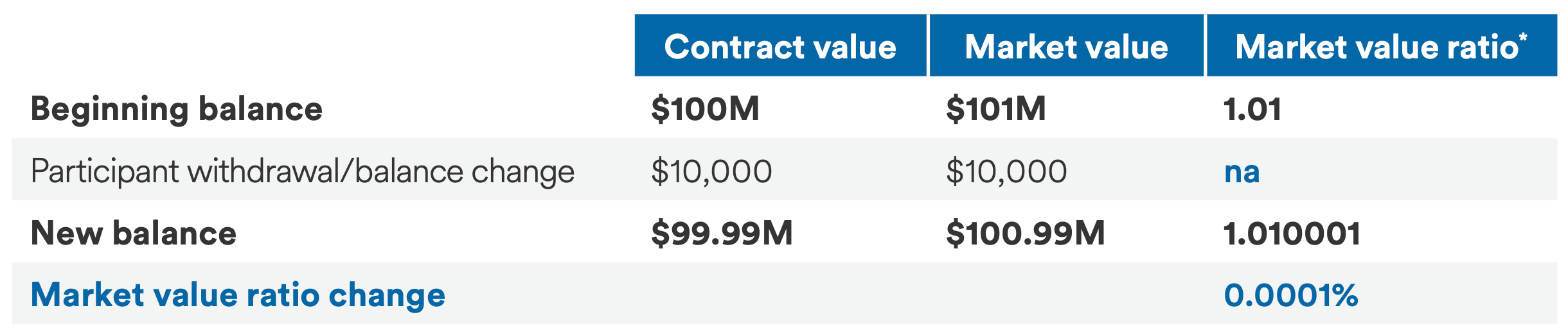

Let’s look at a simple hypothetical example, where the investments of a stable value fund have a contract value of $100,000,000 and a market value of $101,000,000. A participant makes a withdrawal from the participant’s balance of $10,000. Because participant balances are stated at contract value, the total participant balances decrease to $99,990,000, while the market value of the assets decreases to $100,990,000.

Since both the contract value and the market value decrease by the same amount, when they are not equal the market-to-book value ratios change slightly. In our example, the market value ratio increases by .0001%.

Stable value in an unstable economy

During times of market uncertainty and fluctuating interest rates, stable value is uniquely positioned to help protect DC participants’ assets. Stable value has long been a safe haven from market volatility for participants, especially in times of extreme market stress and declining equity markets.

Download this as a PDF

Download*Market value ratios rounded to nearest decimal point for illustration purposes.

Guarantees are subject to the financial strength and claims-paying ability of the issuing MetLife company.

All examples are hypothetical. Individual results may vary.

Group annuity contracts can be issued by Metropolitan Life Insurance Company, 200 Park Ave, NY, NY 10166 or Metropolitan Tower Life Insurance Company, 5601 South 59th St., Lincoln, NE 68516. Like most group annuity contracts, MetLife group annuities contain certain limitations, exclusions and terms for keeping them in force. Ask a MetLife representative for costs and complete details.